Asset allocations are often highly generalized

Most investment guidance is limited to very basic concepts. Recommendations consist of a portfolio mix of a few funds to invest in, with some sort of age-based glide path towards retirement

(so called lifecycle investments).

But most investments have a specific purpose: saving for retirement, a house, kid's education, or preserving wealth. The purpose of an investment can be modelled on historic behaviour. Just like the portfolio.

A portfolio allocation should be linked to that purpose – not generic.

Our mission is to make that linkage explicit and data-backed, but most importantly easily accessible.

Considering your Real Estate

Investment considerations may only consider financial accounts, missing a large part of your portfolio - like the house which you (partially) own and life in. You may not consider selling it, but at the very least your personal financial portfolio should reflect its price developement.

Allocatewise enables you to consider factors outside of your immediate financial portfolio in your considerations.

Investment goal: saving for retirement

The purpose of retirement saving (pension, SIPP, ISA) is clearly defined: covering your future living expenses. It's also the most important financial liability you carry.

There are two main challenges in getting this right:

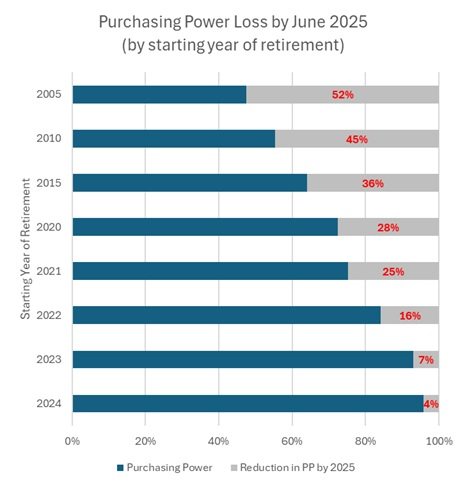

Challenge 1: Living expenses grow with inflation

Standard pension funds and investment managers talk about nominal returns. But your retirement spending grows at least with (and often faster than) inflation. A portfolio that looks fine in nominal terms can still fall short in real purchasing power.

Measuring every return against realised inflation gives a clearer picture of whether your savings are actually keeping pace with your future cost of living.

Challenge 2: Future returns are hard to predict

No one can predict the future. As a result, most retirement strategies rely on static allocation rules – "60/40", risk buckets, or age-based glide paths – that ignore current market conditions.

It's intuitive that what assets cost today should influence how much you hold. For example, bonds with a negative real yield-to-maturity are unlikely to outperform inflation. A good allocation should reflect that reality, not just a rule of thumb.

How we address these challenges

Investments always carry risk, and future returns can never be known in advance. What can be done is to assess historical relationships between assets and their current expected returns and volatility – then use that to generate allocations that are explicitly linked to your retirement spending goals.

Allocatewise does exactly that. The platform takes your living expense trajectory, current asset prices, and historical correlations into account when building and simulating your portfolio.

Allocatewise is not regulated by the Financial Conduct Authority. Access to analysis, allocations, and any opinion expressed here is not financial advice. If you are unsure, please engage a certified independent financial adviser.

How we protect your data.

Allocatewise works with the minimum information needed to run your simulation. We don't connect to your brokerage, store account numbers, or handle sensitive financial credentials of any kind.

You enter tickers, weights, and values. That's it. The platform uses that input to run calculations and return results – no sensitive financial data is retained beyond the holdings needed to build the investment profile.

No bank or brokerage credentials

We never ask for your bank login, brokerage password, or account numbers. There are no open-banking or OAuth connections.

Data never sold or shared

Your portfolio inputs are never sold, shared with advertisers, or used for any purpose outside running your analysis.

Encrypted in transit and at rest

All traffic uses HTTPS/TLS. Data stored in Google Cloud Firestore is encrypted at rest by default.

GDPR-compliant deletion

Delete your account and all associated data at any time. Inactive accounts are automatically removed under our GDPR retention policy.

Ready to explore?

See how this approach applies to your own portfolio and retirement goals.