Challenge and Solution: Inflation as the Benchmark

Saving money to live from later in life ("retirement") is different from general investing. In general investing the benchmark is the risk-free rate paid by governments on their debt. When saving for retirement, the benchmark is the increase in the future cost of living. For simplicity this can be assumed to be inflation - usually expressed as the Consumper Price Index (or CPI). Of course, it is debatable if one's personal consumption costs increase with inflation. But without better alternatives for measuring inflation, using CPI or RPI (in the UK) is better than nothing at all. In addition, nobody knows what their future cost of living will be. The best we can do is to consider current prices for things and extrapolate with inflation.

Looking at retirement savings with consideration to inflation does not only tend to increase the return that is required to exceed the benchmark.

It changes the whole equation!

What matters is the performance against the goal of maintaining a good standard of living, as measured by the portfolio's performance against the CPI.

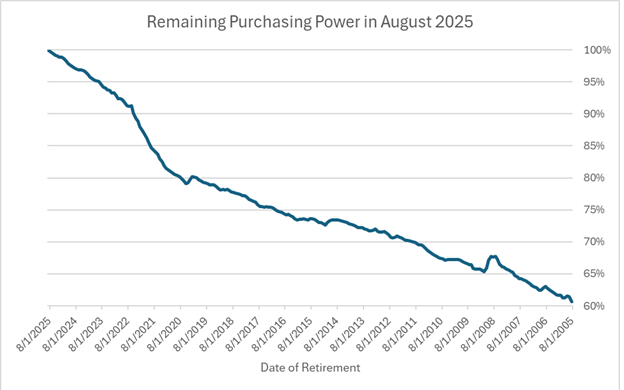

Illustration of the reduction in purchasing power. Since 2005 purchasing power of a Dollar fell by 40% to 60% of it's original value.